The Scholar Behind UMS's Master's Program in IQT

27 July 2026

Prof. Andri Nirwana, S.TH., M.Ag., Ph.D., pioneered the Master of Al-Quran and Tafsir Studies as a first step in strengthening Quranic studies within Muhammadiyah.

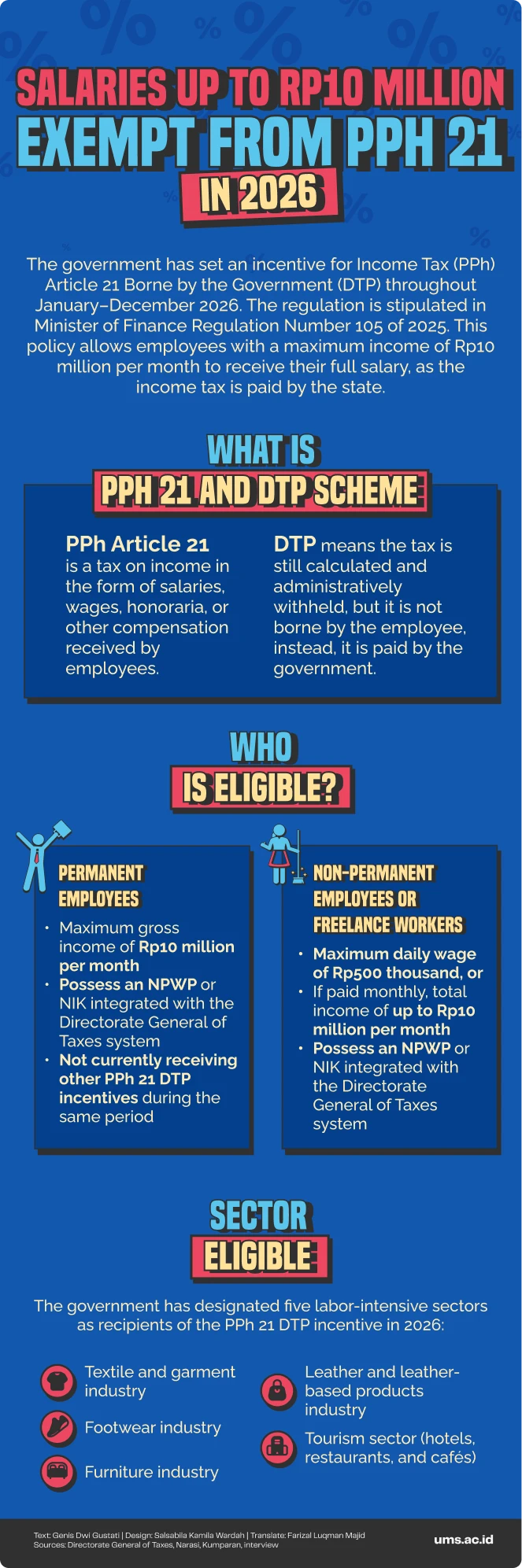

Income Tax Article 21 (PPh 21) has become one of the government’s instruments in responding to economic pressures in 2026. Minister of Finance Purbaya Yudhi Sadewa has implemented this policy for workers earning up to Rp10 million per month throughout 2026 through Minister of Finance Regulation (PMK) Number 105 of 2025, covering five labor-intensive sectors: footwear, textiles and garments, furniture, leather and leather products, and tourism.

The policy is claimed as a fiscal stimulus to maintain public purchasing power. It does not eliminate tax obligations entirely. Instead, the tax is still administratively withheld by employers, but is borne by the government so that it does not reduce workers’ take-home pay.

Lecturer at the Faculty of Economics and Business, Universitas Muhammadiyah Surakarta (FEB UMS), Dr. Kusuma Wijayanto, S.E., M.M., viewed this policy as a positive and practical step in the current economic context. According to him, the government is attempting to be present amid economic pressure by utilizing tax instruments.

“This is a step that I consider positive. The government is using PPh 21 not only as a source of revenue, but as a tool to safeguard the economy and maintain the momentum of labor-intensive sectors,” said Kusuma at Laboratory 5.01, FEB UMS, Thursday (8/1/2026).

The calculation of PPh 21 is a crucial point in this policy. So far, PPh 21 has been a tax that directly cuts into workers’ income, meaning any increase in rates or regulatory changes is immediately felt in reduced disposable income. When this tax is relieved up to the Rp10 million per month threshold, workers automatically receive higher net income without the need for a refund process.

According to Kusuma, the economic logic behind this policy is quite clear. Workers in the lower- to middle-income bracket tend to spend additional income on consumption needs. In other words, every additional rupiah received has the potential to circulate directly in the real sector.

"When PPh 21 tax is exempted for incomes below Rp10 million, people are expected to redirect their earnings toward consumption. They buy goods, spend on daily necessities, and this drives economic circulation,” he explained.

PPh Article 21 has been chosen as a policy instrument amid slowing demand and rising risks of layoffs. Without aggressively increasing state spending, this policy targets active workers, unlike social assistance programs that are passive in nature and not always directly connected to the production process.

The calculation of PPh 21 was deliberately selected due to its direct linkage to employment. The five sectors receiving the incentive are known as labor-intensive industries, employing large numbers of workers and being relatively vulnerable to economic shocks.

Kusuma believed that the focus on these sectors is not without reason. The textile, footwear, and tourism industries have faced heavy pressure over the past few years, ranging from declining demand and high production costs to layoffs in various regions.

“These five sectors indeed absorb a large workforce. Through this policy, the government aims to keep industries running and to curb layoffs,” he said.

However, Kusuma cautioned that limiting the incentive to only five sectors could potentially raise issues of horizontal equity. Workers in other sectors with the same income levels would still be required to pay taxes, despite being similarly affected by economic conditions.

“This is something that needs attention. Indonesia has many sectors, not just five. We should avoid the emergence of jealousy or a sense of injustice. Ideally, the government should provide a clear explanation, we will wait for the reasoning,” he said.

From the business perspective, this policy could potentially give employers a justification to hold back wage increases. After all, wage increases for workers remain something that should be considered, even when taxes are borne by the government.

Tempo reported that the President of the Nusantara Confederation of Labor Unions, Ristadi, warned that the majority of workers in labor-intensive industries fall into the category of workers whose income is below the non-taxable income threshold (PTKP). With salaries below Rp54 million per year or Rp4.5 million per month, the incentive is therefore considered to have only a limited impact on purchasing power and to benefit only a small portion of workers.

A similar concern was expressed by the President of the All-Indonesia Workers Union Association, Mirah Sumirat. Quoted by Tempo, Mirah cautioned that the PPh 21 tax exemption policy should not be used by employers as a reason to withhold or delay wage increases on the grounds that part of workers’ income is already supported by the state. Although the policy provides a short-term increase in net income, workers’ welfare remains at risk if tax incentives instead weaken employers’ commitment to providing decent wages.

Income tax calculators are likely to be accessed more frequently by workers and companies throughout 2026. Although the tax is borne by the government, employers are still required to calculate, administratively withhold, and report PPh 21 in the Monthly Tax Return (SPT Masa).

“What does this mean? From an accounting and administrative perspective, since I am an accounting lecturer, the burden on companies does not disappear entirely,” Kusuma explained.

Kusuma highlighted this challenge as one of the government’s pending tasks. Without a well-organized payroll system or proper administrative systems for salary payments, along with adequate human resource capacity, the policy risks causing reporting errors or even irregularities.

“Administratively, companies still have to calculate and report it. If supervision is weak, there is a risk of misclassification or manipulation to meet the exemption criteria,” he said.

On the positive side, the policy encourages tax compliance. The requirement to have a Tax Identification Number (NPWP) or a National Identification Number (NIK) integrated with the Directorate General of Taxes (DJP) effectively forces workers and companies to enter the formal tax system. In the long term, this can strengthen the national tax database.

PPh Article 21 is one of the major contributors to state revenue. If this incentive is extended without proper evaluation, the risk of fiscal pressure cannot be ignored.

“The exemption of PPh Article 21 is indeed not a long-term policy. However, it is a significant contributor to state revenue. If it is reduced or continuously borne by the government, there must be compensation through economic growth,” he said.

Therefore, regular evaluation is key. The government needs to assess whether this policy truly increases consumption, suppresses layoffs (PHK), and drives growth in labor-intensive sectors. If not, a different and more effective formula will be needed.

Kusuma also emphasized the importance of public trust. According to him, Indonesian society is basically tax-compliant. The issue is not whether people are willing to pay taxes, but to what extent the state can demonstrate that taxes are managed fairly and transparently.

“Taxation is about trust. The government must be able to provide a sense of security that the taxes paid do indeed return to society,” he warned.

In the short term, the policy is considered relevant and contextual. However, as Kusuma cautioned, fiscal stimulus cannot stand alone.

This PPh Article 21 policy still carries the risk of creating new problems if implemented without strong oversight, technical clarity, and continuous evaluation. “If the economy improves, this policy can serve as a bridge. But if not, the government must be brave enough to evaluate it and seek another formula,” he concluded.

Writer: Genis Dwi Gustati

Translator: Farizal Luqman Majid

Editor: Al Habiib Josy Asheva

Prof. Andri Nirwana, S.TH., M.Ag., Ph.D., pioneered the Master of Al-Quran and Tafsir Studies as a first step in strengthening Quranic studies within Muhammadiyah.

Nothing’s more special than reading curated news just for you.

Subscribe to the UMS Newsletter for free today.